By Matt Read, Super Members Council Australia Head of Strategic Communication

Last updated 27 April 2026

| Campaign update We did it! Payday super laws – a gamechanger to tackle unpaid super – passed Parliament on 4 November 2025. The Council commends all Parliamentarians for swiftly passing the laws first promised over two years ago. See more information below about SMC campaign for payday super laws to help stamp out unpaid super. |

Every year, billions of dollars in superannuation goes unpaid to Australian workers. For those affected, this can mean more than $30,000 less in super savings by retirement, forcing more reliance on the age pension.

A key cause of this challenge are laws made in the 1990s that only require employers to pay super contributions quarterly, out of alignment with the payment of wages. Most workers assume their super is paid with wages because that’s what appears on their payslip.

The good news is, these laws are changing soon, and employers will be required to pay super to their employees at the same time.

This will help to reduce the amount of unpaid super, however there is still more that can be done – and there’s still a risk your super could not be paid if you don’t keep an eye on your payments.

Learn more about the new payday super laws and what you can do if you think your super has been underpaid.

On this page:

- What counts as unpaid super?

- How often does superannuation need to be paid? Super entitlements at a glance

- The payday super solution will be effective

- How do I know if I’m a victim of unpaid super?

- Penalties for not paying superannuation

- Reporting unpaid super (step by step)

- Unpaid super is deepening retirement inequality for women

- What else can be done to solve the unpaid super problem?

- FAQs

What counts as unpaid super?

Unpaid super is any superannuation an employer was legally required to pay but didn’t. Under the super guarantee, most employers must contribute 12% of your earnings into your super fund.

If they don’t pay this, don’t pay the full amount, or pay it late, it can be considered underpaid super.

How often does superannuation need to be paid? Super entitlements at a glance

Under current laws, employers are only required to pay super quarterly, not with every pay cycle. That four-month window can be enough for some employers to fall behind with payments, and for workers to be none the wiser.

Super is due to be paid by an employer four times a year, on these dates:

| Quarter | Period | Payment due date |

| 1 | 1 July – 30 September | 28 October |

| 2 | 1 October – 31 December | 28 January |

| 3 | 1 January – 31 March | 28 April |

| 4 | 1 April – 30 June | 28 July |

The amount you’re entitled to receive is 12% of your Qualifying Earnings, which generally includes your ordinary time earnings (OTE)—such as base salary, commissions, bonuses, and paid leave – as well as commissions, salary sacrifice amounts, and others. For a full list of what constitutes Qualifying Earnings, see here.

From 1 July 2026, payday super will be introduced, requiring employers to pay superannuation at the same time as wages, which will make it easier for workers to track their contributions in real time.

The scale of unpaid superannuation might surprise you. Download our research on solving the unpaid super crisis to learn more.

The payday super solution will be effective

As mentioned, the Australian Government has passed laws that will require employers to pay their employees’ super at the same time as their salary and wages from 1 July 2026.

Payday super will make it easier to identify that super hasn’t been paid. Paying super more frequently also generates higher super balances through additional investment returns and compound interest on super paid fortnightly instead of quarterly.

That will benefit a quarter of workers who are currently paid super quarterly. A worker on median wages could have an extra $7,700 at retirement.

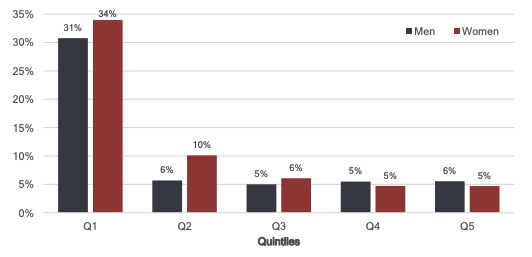

While this is an important step forward in solving the problem of unpaid super for Australians, there is still more work to be done.

Projected percentage of super balance at retirement lost to unpaid super, by wage quintile

How do I know if I’m a victim of unpaid super?

The quickest way to check is to compare what you should be receiving against what’s actually landing in your account. It’s a good habit to get into.

Research shows up to 40% of workers never check their super contributions.

The ATO employee SG entitlement calculator makes it easy to work out your entitlement in a few clicks.

Penalties for not paying superannuation

Employers who don’t pay superannuation on time face serious consequences under Australian law.

If an employer misses the quarterly deadline, they become liable to pay the superannuation guarantee charge (SGC).

The SGC is calculated differently from regular super contributions and is calculated on the shortfall amount, notional earnings, a choice loading if relevant and an administrative amount that can be reduced depending on the employer’s compliance with the laws.

Unlike regular super contributions, it’s also not tax-deductible for the employer.

Employers found to have deliberately avoided their super obligations can face additional penalties on top of the SGC. In serious cases, the Australian Taxation Office (ATO) can take further action, including audits and legal proceeding.

Reporting unpaid super (step by step)

If you think your employer hasn’t been paying super correctly, here’s how to work through it.

Step 1: Check you’re entitled to super

Before anything else, use the ATO’s am I entitled to super? tool to check you’re covered.

Step 2: Track your contributions

Log in to your super fund account or check out your member statements to see what contributions have been received.

If you’re unsure, it’s worth asking your employer directly about when they paid, how much, and which fund it was paid to. Sometimes contributions have been paid to the wrong fund, which is a separate issue to address.

Step 3: Work out what you should’ve received

Use the ATO’s estimate my super calculator to work out your super entitlement based on your earnings. Comparing this to what’s actually in your account will confirm whether there’s a shortfall.

Step 4: Check with your employer

In many instances non or incorrect payment is a mistake that can be rectified quickly and with interest.

Lodge a report with the ATO

If you’ve worked through the steps above and confirmed your super hasn’t been paid correctly, you can lodge a report using an ATO online tool.

Once you’ve lodged, the ATO will investigate and let you know by letter or email if it’s able to collect any unpaid super and distribute it to your fund.

The process can take time, and not every case results in a recovery, but reporting it is the right thing to do.

Other options if you need more support

Reporting to the ATO is the right first step, but it’s not your only option.

The Fair Work Ombudsman can help if you’re also missing wages or other entitlements, and can pursue your employer on your behalf, including through the courts.

Unpaid super is deepening retirement inequality for women

Women across Australia continue to miss out on super due to time spent out of the paid workforce to care for children and other family members. This contributes to an overall gender gap in super balances, which leads to working women in Australia retiring with a quarter less super than men.

This structural inequity also means women suffer more acutely from the scourge of unpaid super. The smaller your balance, the bigger a difference each dollar of unpaid super makes.

Missing out on super – which is a legal workplace entitlement in Australia – dramatically erodes women’s super by retirement, magnifies existing inequity, and erodes women’s future financial security.

This report focuses on how fixing unpaid super will benefit women in retirement.

Every unpaid contribution adds up. And for women, who already retire with 25% less super than men on average, that gap has real consequences. Read our mind the gap report to understand the bigger picture.

What else can be done to solve the unpaid super problem?

In addition to payday super legislation, the Government should also establish a stronger Australian Tax Office (ATO) compliance regime. That includes setting the originally promised targets and committing to support workers to reclaim their legal super entitlements in the case of insolvencies.

Effective legislation backed by a robust compliance regime is the only way to ensure millions more Australians get their full super entitlements.

Stay up to date with superannuation news and policy. Subscribe to receive updates straight to your inbox.

FAQs

-

Does superannuation get paid on overtime?

Generally, no. The Super Guarantee is calculated on Qualifying Earnings (QE), which usually excludes overtime. Superannuation may be payable on overtime that is part of your ordinary hours of work or regularly rostered overtime. The rules can vary depending on your employment agreement. If you’re uncertain, check with your super fund or employer.

-

What is the time limit to claim unpaid super?

The ATO can generally pursue unpaid super for up to four years from when it was due. If you suspect you have unpaid contributions, it’s worth checking sooner rather than later.

-

Can casual workers claim unpaid super?

Yes. Most casual employees are entitled to super contributions, provided they meet the eligibility criteria. The Super Guarantee applies regardless of whether you work full-time, part-time or casually.

-

What if my employer can’t afford to pay my super?

Your employer’s financial situation doesn’t change their legal obligation to pay your super. If your employer is struggling financially or has gone into administration, the ATO may still be able to recover unpaid contributions. Contact the ATO or seek advice from a financial counsellor.

About the author

Matt Read

Super Members Council Australia Head of Strategic Communication

Matt is responsible for strategic stakeholder engagement, communication, and advocacy at SMC and has over 20 years of experience as a strategic communications leader.

See more about Matt: