By Misha Schubert, Super Members Council Australia CEO

Last updated 16 April 2026

Super has transformed the lives of millions of Australians. But right now, Australian women are still retiring with a third less super than men.

The gender super gap has narrowed over the years with increased female labour force participation, but progress has slowed while other key factors contributing to the problem remain unaddressed.

On this page:

- The reality of the gender superannuation gap

- What the gender super gap looks like in Australia

- The big question: Why Australian women retire with less superannuation

- The real cost of the gender super gap

- Helping to close the gender super gap in the short-term

- Longer-term fixes also needed

- Superannuation strategies for women

- Where to access support and resources

The reality of the gender superannuation gap

By their early 60s, the median super balance for women is around $51,000 lower than it is for men. Women are also more likely to reach retirement with little or no superannuation at all.

This is the reality of the gender super gap in Australia. And it doesn’t happen by chance. It builds slowly over a lifetime shaped by lower average wages, time spent out of the workforce caring for others, and a superannuation system originally designed around uninterrupted, full-time work.

What the gender super gap looks like in Australia

Although the compulsory superannuation system that we know in Australia as Superannuation Guarantee started for both men and women in 1992, the gender super gap becomes clear when you look at superannuation across different life stages.

The table below shows the median balances for men and women across different age groups in Australia (2022–23). The problem is persistent from the early years of working life through to retirement, women have less super than men.

| Age group | All persons | Male | Female | Gap |

| 20s | $12,700 | $13,000 | $12,400 | 5% |

| 30s | $53,600 | $60,000 | $47,900 | 20% |

| 40s | $114,700 | $135,100 | $96,700 | 28% |

| 50s | $175,300 | $212,400 | $143,100 | 33% |

| 60s* | $222,200 | $254,600 | $189,900 | 25% |

| All 20–64 | $62,100 | $72,500 | $53,800 | 26% |

Want to understand the full picture?

Download our Mind the Gap report, which focuses on how fixing the problem of unpaid super will support more women as they near retirement.

The big question: Why Australian women retire with less superannuation

The reasons women retire with less superannuation are complex and closely tied to how work, pay and caregiving are structured in Australia.

The gender pay gap

Women earn less than men on average, which means lower super contributions throughout their careers. Because super is calculated as a percentage of wages, earning less over time leads to a smaller super balance.

Career breaks and part-time work

Women are more likely than men to take time out of the workforce or reduce their hours, often to care for children or older family members. Time away from paid work means time without employer super contributions.

Caring responsibilities

Unpaid caregiving is still disproportionately carried by women in Australia. Whether it’s looking after young children, an ageing parent, or a family member with a disability, time spent caring often comes at the cost of earning income and building super.

Later-in-life disruptions

Events such as separation, family violence, menopause or unexpected early retirement can significantly affect a woman’s ability to keep working. Many women leave the workforce earlier than planned, which reduces the time available to build retirement savings.

Gaps in super coverage

Some workers still fall through gaps in the super system. Nannies, housekeepers and carers — roles predominantly filled by women — have historically been excluded from compulsory super in some situations. Younger workers under 18 have also faced exclusions due to under-18 workers being ineligible for super unless they work more than 30 hours a week with the same employer. Young women are more disadvantage by this out of date rule because they typically do more part-time work than men.

Learn more about the history of superannuation over on our superannuation basics and history page.

The real cost of the gender super gap

Having less super in retirement doesn’t just mean a smaller number in an account. It can mean less independence, fewer choices, and greater reliance on others at a time in life when financial security matters most.

Women who retire with lower super balances are more likely to depend on the Age Pension, more likely to be renting rather than owning their home, and more exposed to financial hardship if something goes wrong.

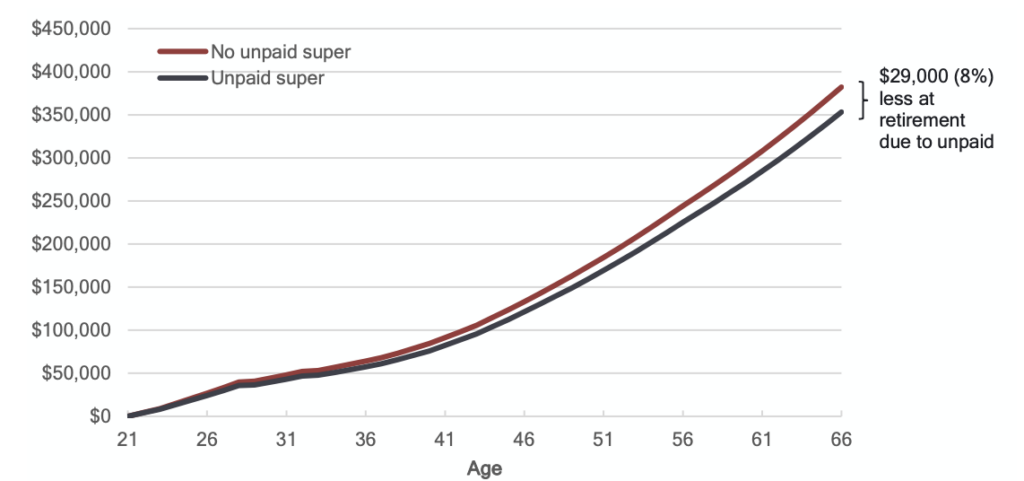

Unpaid super is another issue that affects women more than men. Our research found that women are being made $26,000 poorer in retirement due to unpaid super. This is money they were legally owed but never received.

Helping to close the gender super gap in the short-term

SMC modelling shows a few targeted changes would go some way to closing the gender super gap. These include improvements to the Lower Income Superannuation Tax Offset (LISTO) and paying super on the Commonwealth parental leave, which could boost the super balances of the lowest paid women by 21 per cent.

In March 2024, the Australian Government announced its decision to pay super on its parental leave scheme. The SMC congratulates the Government for this historic decision, which is due to take effect on 1 July 2025. Paying super on the Commonwealth Parental Leave Pay Scheme will leave a mother of two $12,500 to $14,500 better off at retirement. With the typical woman retiring with around $50,000 less than their male counterparts, this would make a meaningful reduction in the gender super gap.

In early 2026 the Australian Government passed laws to fix problems with the LISTO, which will boost the super of 1.3 million of the nation’s lowest-paid workers, who are mostly women. For a woman who earns the minimum wage across her whole working life, our modelling shows it could deliver up to $60,000 more in her super by retirement – dramatically lifting her income.

Longer-term fixes also needed

The gender super gap is also caused by broader issues, which we should be addressing longer-term: women’s lower workforce participation rates, the fact that highly feminised industries and jobs continue to attract lower wages, and social norms around unpaid caring responsibilities.

We are advocating for the following longterm fixes to address the super gender gap:

- Close gendered loopholes in super coverage, including through payday super reforms, and by paying super to all workers, including nannies, housekeepers, carers, and under-18 workers.

- Remove barriers to women’s workforce participation by boosting access to childcare and aged care and strengthening workplace flexibility.

- Enable fairer splitting of superannuation in divorce settlements when they are handled out of court.

- Boost Commonwealth Rent Assistance to give immediate help, and invest in new social housing over the medium-term, to protect vulnerable older women who rent or are at risk of homelessness. SMC will advocate for a broad suite of policies to help close the gender super gap.

SMC will continue to look at all the factors contributing to this issue – large and small – and is committed to working with all Governments in the future to find ways to keep lifting the retirement savings of women to close the equity gap.

Superannuation strategies for women

While systemic change is needed to fully close the gender super gap, there are practical steps women can take to strengthen their super balance over time.

Make voluntary contributions

If your budget allows, topping up your super with voluntary contributions can help boost your retirement savings. These may be concessional contributions (from pre-tax income) or non-concessional contributions (from after-tax income).

Take advantage of the government’s co-contribution scheme

If you earn below a certain threshold and make a personal after-tax contribution to your super, the government may add to it. This is known as the superannuation co-contribution.

Ask your partner to contribute to your super

If you’ve taken time out of work or reduced your hours, your partner may be able to contribute to your super on your behalf. This is called a spouse contribution, and in some cases, your partner may be eligible for a tax offset.

Keep track of your super

Lost or unclaimed super is a common issue in Australia. You can check your super balance and search for lost accounts through the ATO via myGov. Consolidating multiple accounts can also help reduce duplicate fees.

Check your insurance coverage

Many super funds include life insurance and income protection insurance. If you’re returning to work after a career break, it’s worth checking that your cover is still active and still suits your needs.

Superannuation for self-employed women: Key tips

- Make a super contributions plan: If you’re self-employed, you won’t receive mandatory employer contributions to your super, so it’s important to have a plan in place to make your own contributions to your super fund.

- Take advantage of tax benefits: Personal contributions may be tax-deductible, reducing your taxable income.

Where to access support and resources

If you want to better understand your super and explore ways to improve your retirement savings, there are several useful places to start.

Our research

We regularly publish research and policy analysis on women and superannuation, including our Mind the Gap report exploring the gender super gap in Australia.

Your super fund

Your fund is often the first place to go for help. Most super funds offer online tools, calculators and member services to help you understand your balance, investment options and insurance cover.

MoneySmart

Run by ASIC, the Australian Government’s MoneySmart website offers free, independent guidance on managing and growing your super, including calculators and a retirement planner.

ATO via myGov

Through your myGov account, you can view all your super accounts, search for lost super and consolidate multiple accounts.

Subscribe to our Super Wrap newsletter to receive curated super updates and to be notified of upcoming events.

About the author

Misha Schubert

Super Members Council Australia CEO

Misha’s career has combined deep expertise in public policy debates and policy advocacy, executive leadership, board directorships and governance, Government relations, member and stakeholder engagement, speechwriting, communications, and journalism.

See more about Misha: