When investment markets fall and your super balance drops, the impulse to ‘do something’ can be overwhelming. You might feel tempted to switch from, say, growth options to cash or conservative investments to ‘protect what’s left’. But here’s the uncomfortable truth: switching during a downturn often locks in losses and means you miss the recovery.

Australia’s super system is designed to grow your retirement savings long-term, even as markets experience volatility. It’s good to remember that volatility is just noise; diversification and a long-term investment timeframe is your seatbelt.

What ‘locking in losses’ really means

When markets fall, the value of your super drops – but only on paper. The loss only becomes real when you sell.

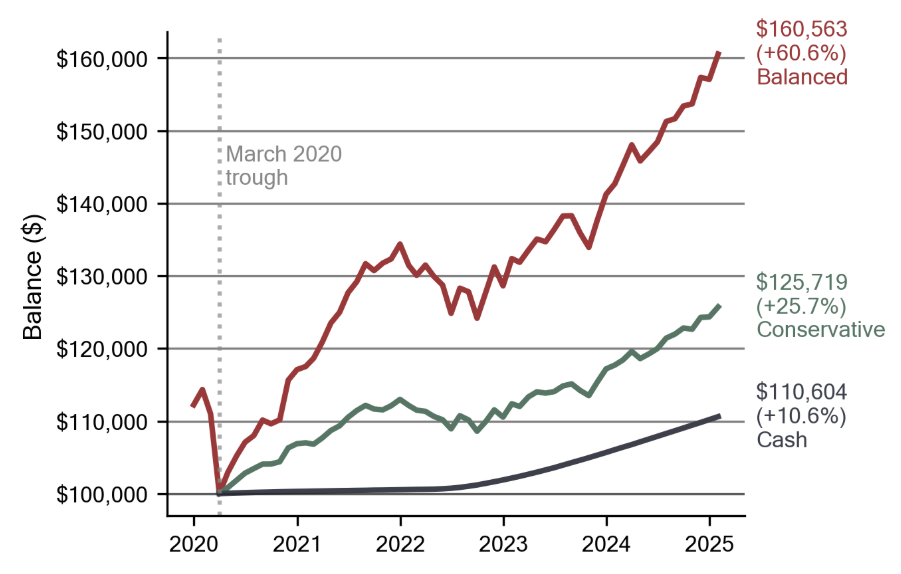

Here’s a simple example. During COVID-19, markets fell and at the bottom of the market Sarah and her friend each had $100,000 in a balanced super option. At that point Sarah panicked and switched everything to cash. Five years later, markets had rebounded and her friend who stayed invested in a balanced option has a balance around $161,000.

But by switching when her balance was down, Sarah sold low and turned a temporary paper loss into a permanent real loss, missing the rebound. Sarah now only has about $111,000 in her super, putting her about $50,000 (50 percentage points) worse off than her friend.

Figure 1 – Switching at the Trough – COVID-19

More recently, in March 2025 when the US started imposing tariffs and markets dropped, if a member switched to cash they would be around $7,000 (7 percentage points) worse off after just one year.

In super, ‘time in the market’ matters more than trying to ‘time the market’

How diversified super options work

Investment options are the different ways your super fund invests your money. Most Australians’ super is invested in balanced options with investments diversified across different asset classes, industries and geographies.

This diversification is your first line of defence against volatility.

- Balanced options: Comprise a mix of growth assets (shares, property) and defensive assets (bonds, cash). Moderate volatility and solid long-term returns makes this the default for most Australians.

- Conservative options: Offers a higher allocation to cash and bonds. Lower volatility might give you more peace of mind so long as you are comfortable with forgoing returns in the future. .

- Growth options: Allocates more to shares and property. Higher short-term volatility and historically stronger returns over 10+ years makes this suited to younger members.

Super is typically highly diversified. Only a portion of your super is invested in any single economy or share market. Funds spread investments across individual stocks, industries, countries and asset types – and buy into the market gradually as markets move up and down. When one market falls sharply, other parts of your portfolio may hold steady or even rise.

That means when you see news headlines of a share market sell-off, it usually doesn’t translate directly to your super balance because of the way your super fund has diversified your investments.

Short-term noise vs long-term goals

This week’s market falls will have little impact in 20 years or more when today’s super fund members will start to think about retiring. Money that remains in super for many years enables short-term losses to be recouped.

Historical performance backs this up. Profit-to-member funds have returned strong long-term returns (well over 7 per cent per year on average over 20 years plus1) despite the downturns – by staying invested through volatility, not by avoiding it.

When choosing a super fund, focus on fees, suitable insurance cover and returns over five years or more. A fund that’s down 8 per cent this year but averaged 9 per cent annually over the past decade is still a solid performer. That’s why short-term returns tell you almost nothing about quality – they mostly reflect recent market noise.

A decision checklist before you switch

If you’re considering switching investment options during a downturn, pause and ask yourself these questions:

- Why am I switching? If the answer is ‘because my balance is down’, that’s a warning you might be about to lock in losses.

- What’s my time horizon? If retirement is more than a few years away, switching to conservative options likely hurts your long-term outcome. You still have a long investment timeframe.

- What’s my actual risk tolerance? Are you genuinely uncomfortable with volatility, or reacting to a temporary drop? There’s a difference between ‘I never want to see my balance fall’ (suggests conservative options might suit you long-term) and ‘I’m panicking because markets just fell 10%’ (suggests you need to sit tight).

- Have I checked the fees? Some conservative and cash options have fees that eat into your returns. Make sure you’re not paying high fees for low returns.

- What happens to my insurance? Some investment options include different insurance arrangements. Switching might affect your cover so check before you move.

- Have I sought advice? If you’re seriously considering switching, talk to a financial adviser or your super fund’s advice team. They can help you understand whether switching makes sense.

When might switching make sense?

Switching can be the right choice when there are legitimate reasons to change investment options:

- Life stage changes: You’re close to retirement and want to gradually reduce risk. This should be planned and gradual – not a reaction to a market fall.

- Sustained strategy drift: Your fund’s investment approach has fundamentally changed over several years and no longer suits your goals. This is about long-term trends, not short-term volatility.

- Major life changes: You’ve inherited money, your income has changed significantly, or you have new financial responsibilities that genuinely change your risk capacity.

It’s worth getting professional advice before acting on any changes to your super options.

The calmer approach

During periods of market volatility, super switching in response to short-term movements often does more harm than good. Ride it out by trusting the system you’re already in – your super fund employs highly skilled investment experts to navigate these ups and downs. They plan for volatility because it’s part of the super lifecycle.

Super Members Council reminds Australians that our super system is well placed to ride out volatility. You can always speak to your super fund’s advice team with any concerns. But with super a long-term policy by design, members should feel confident to stay invested and give super time to recover when markets cycle upwards again.

FAQs

Q. Should I switch to cash or conservative options when markets fall?

A. For most working-age Australians, no. Switching after markets have already fallen can lock in losses super members may never recover from. Super is a long-term investment designed to recover from short-term volatility.

Q. How do I know if my investment option is right for me?

A. Consider your time until retirement and your comfort with volatility. If retirement is more than a few years away, balanced or growth options typically suit most people. If you’re within a few years of retirement, gradually moving toward more conservative options can make sense – but this should be planned, not reactive. Your super fund’s advice service can help you assess what suits your circumstances.

Q. What’s the difference between balanced vs growth super options?

A. Balanced options mix growth assets (like shares and property) with defensive assets (like bonds and cash), targeting moderate long-term returns with moderate volatility. Growth options have higher allocations to shares and property, accepting higher short-term volatility for potentially higher long-term returns. Balanced suits most working Australians, while growth suits younger members comfortable with more ups and downs.

Q. How long does it typically take for super to recover after a market downturn?

A. Historical data shows balanced super options typically recover within 1-3 years after significant market falls, including the 2008 Global Financial Crisis and the 2020 COVID crash. The key is staying invested – those who switched to cash during downturns often took much longer to recover or never fully made back their losses.

Q. Should I check my super balance regularly during volatile times?

A. Super is designed for long-term investing, not daily monitoring which can increase anxiety without adding value. Consider checking once or twice a year and if your balance is down, remember this is temporary volatility – not a signal to switch.

References

1. Australian Prudential Regulation Authority 2025

General information only. Consider getting advice from a licensed adviser or your super fund.