By Misha Schubert, Super Members Council Australia CEO

Last updated 15 April 2026

Starting a first job is usually an exciting time for under-18s – earning money for the first time and getting a taste of financial independence.

It’s a big milestone for many Australians, but there’s an important aspect to work as an under-18 that is often overlooked: superannuation.

On this page:

- Eligibility and rules for under-18s

- The 30-hour rule: out of touch with the modern worker

- Choosing a super fund for young workers

- Managing super under 18

- For employers with under-18 workers

- FAQs

Eligibility and rules for under-18s (including casual employees)

In Australia, employees are entitled to super contributions under the Superannuation Guarantee, and under-18s are no exception.

The one difference is an added condition: employer contributions are only required when an under-18 worker works more than 30 hours in a week.

Understanding the Super Guarantee for under-18 workers

The Super Guarantee (SG) is the minimum percentage of wages an employer is required to contribute to a super fund.

It’s the same amount regardless of age—and, as of 2025, the Super Guarantee rate is 12%.

Want to understand more about how the super system works? Head to our superannuation basics and history page.

The 30-hour rule: out of touch with the modern worker

This rule has been part of Australia’s super system for decades, but its original purpose is no longer relevant.

Introduced in 1992 at the commencement of the modern super system to shield employers from having to pay super to very-low income workers whose low-balance accounts would likely be eroded by fees and insurance premiums.

Today, fee caps and stronger protections mean that justification no longer holds up.

What we’re left with is a rule that creates confusion for teenagers, adds complexity for businesses, and leaves a gap in superannuation that can cost young workers real money over time.

What the rule means in practice

The 30-hour threshold is harder to administer than it might seem. In industries where casual work is common and hours shift week to week, employers must track each under-18 worker individually to determine whether the threshold has been met.

This can lead to super accounts being opened and closed several times before a worker even turns 18.

Removing the threshold would give employers a consistent, straightforward approach to superannuation for all workers, regardless of age.

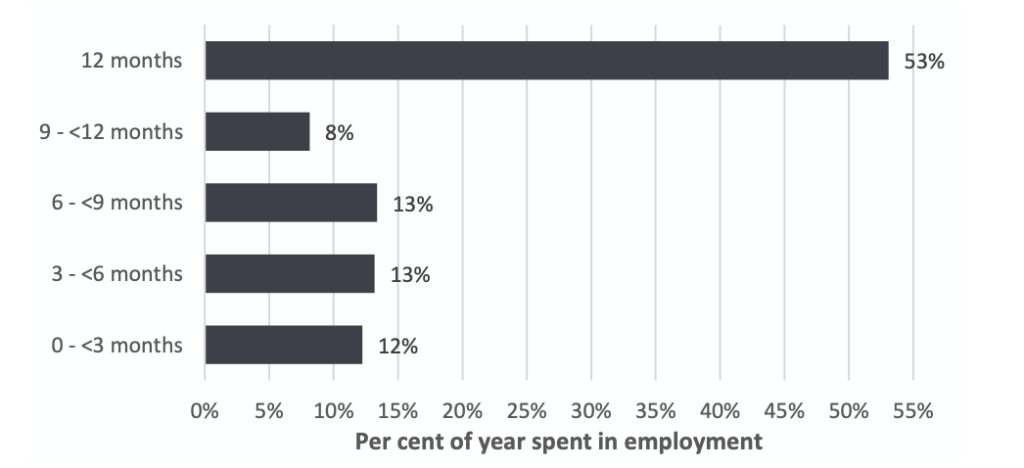

The numbers tell the story

The scale of the problem is significant. Around 505,000 under-18 workers were excluded from super in 2024–25, missing out on a combined $368 million in contributions.

And the idea that under-18s only work for pocket money doesn’t hold up. More than half (51%) work across the whole year or most of it.

For a typical teenager working for at least two years, paying super from day one would mean almost $2,200 in their super account by the time they turn 18.

By retirement, that figure is projected to grow to almost $10,000 in today’s dollars, demonstrating that the earlier super starts building, the harder compounding works.

And for a median wage earner, compound earnings account for between two-thirds and three-quarters of a super balance at retirement.

Australians want change

Support for scrapping the 30-hour rule is strong and consistent.

85% of Australians believe anyone in paid work should receive super, and that’s a view shared across all parts of the community.

Making super universal for under-18 workers would also reduce long-term reliance on the Age Pension, easing pressure on the federal budget for everyone.

For the full picture on super for under-18s, download our guaranteeing a super start to work report.

Choosing a super fund for young workers

Selecting the right super fund early on can make a significant difference to a retirement balance.

When starting a new job, an employer will ask for a super fund nomination, giving the choice of listing your current fund, switching to the employer’s default fund, or choosing a different one altogether.

Without a nomination, super goes into the employer’s default MySuper option.

While there are many types of super funds, not all have strong long-term returns.

What to look for when choosing a fund

A few key fund features can hugely impact your retirement savings.

- Long-term performance.

Super is a long-term investment, so consistent long-term performance matters more than short-term spikes. - Low fees.

The most common fees include administration and management fees. While the amounts may seem small, these annual costs can eat into future savings over time. - A fund run to benefit its members.

Funds that return profits to members rather than shareholders have historically delivered better long-term returns.

All of the Super Members Council member funds are profit-to-member funds. Learn more about SMC member funds.

A small difference in fees or performance makes a big difference over the long term. Analysis by SMC shows a 1% higher fee or lower investment return p.a. can equate to up to $128,000 difference in balance at retirement (age 67).

Managing super under 18

Super is locked away until the preservation age of 60, and in all but the most exceptional circumstances, that’s when it can first be accessed. For example, there are some situations where early access is possible, including severe financial hardship, terminal illness or permanent incapacity.

Either way, managing super well from the start can make a meaningful difference over time. The following content provides more detail on how to manage your super effectively.

How super works

Making super work harder

A few simple habits can help make the most of super from the start.

Consolidate accounts

Working multiple jobs can mean ending up with multiple super accounts, each charging fees. Checking for lost or duplicate accounts through myGov and consolidating into one fund is a straightforward way to avoid unnecessary costs.

Keep details up to date

Super funds need a current tax file number (TFN), up-to-date contact details and nominated beneficiaries. Without a TFN, employer contributions may be taxed at a higher rate.

Make voluntary contributions

Even small additional contributions early on can have a significant impact over time, thanks to compounding growth.

Check contributions are being paid

It’s worth checking regularly that employer contributions are landing in the fund, through the fund’s member portal or myGov. If something looks wrong, the first step is to raise it with the employer, and then the ATO if needed.

For employers with under-18 workers

All under-18 workers deserve to have their super paid correctly, and that starts with employers knowing the rules.

Super must be paid for any employee under 18 who works more than 30 hours in a week—whether they are casual, part-time or full-time.

Why paying super to all under-18 workers matters

Under-18 workers are among the lowest-paid in Australia. Many are in roles where they have little negotiating power and limited awareness of their workplace rights.

SMC research shows that those excluded from the Super Guarantee are disproportionately female, and that the gap compounds over time. Paying super regardless of hours would help make sure young Australians, especially young women, don’t start their working lives already behind.

For employers, the cost is small, but for a young worker, it can make a meaningful difference to their retirement decades down the track.

Payday super reforms

From 1 July 2026, super must be paid at the same time as wages. Updating payroll processes ahead of time will make the transition smoother and help ensure young workers receive their entitlements on time.

Stay up to date with superannuation news and policy changes. Subscribe to receive updates straight to your inbox.

FAQs

-

What is the minimum age to open a super account in Australia?

There is no minimum age to open a superannuation account in Australia. If under 18 and working, an employer may be required to contribute to a super fund. Many super funds allow young people to open an account directly, even before starting work.

-

Do you get superannuation if you work part-time under 18?

It depends. Under-18 workers are entitled to super contributions when working more than 30 hours in a week, regardless of whether the work is casual, part-time or full-time. If working 30 hours or fewer in a week, the employer is not required to pay super.

-

Can parents contribute to their child’s super?

Yes. Parents and family members can make voluntary contributions to a child’s super fund. These are called non-concessional (after-tax) contributions. While the amounts may be small early on, they can grow significantly over time thanks to compounding returns.

-

What happens to super if you change jobs under 18?

Super stays with the worker when jobs change. Thanks to stapling reforms introduced in 2021, a super account is linked to the individual — not the employer. When starting a new job, the employer will pay into the same fund unless advised otherwise. This helps avoid multiple accounts and duplicate fees.

-

Can minors have a super account?

Yes. There is no minimum age requirement to hold a super account in Australia. Young workers can be members of a super fund, and most major funds welcome younger members.

About the author

Misha Schubert

Super Members Council Australia CEO

Misha’s career has combined deep expertise in public policy debates and policy advocacy, executive leadership, board directorships and governance, Government relations, member and stakeholder engagement, speechwriting, communications, and journalism.

See more about Misha: